Long-term relationship between energy consumption and GDP in Latin America: an empirical assessment using panel data

Main Article Content

Keywords

Energy Consumption, Economic Growth, Production Function, Panel.

Abstract

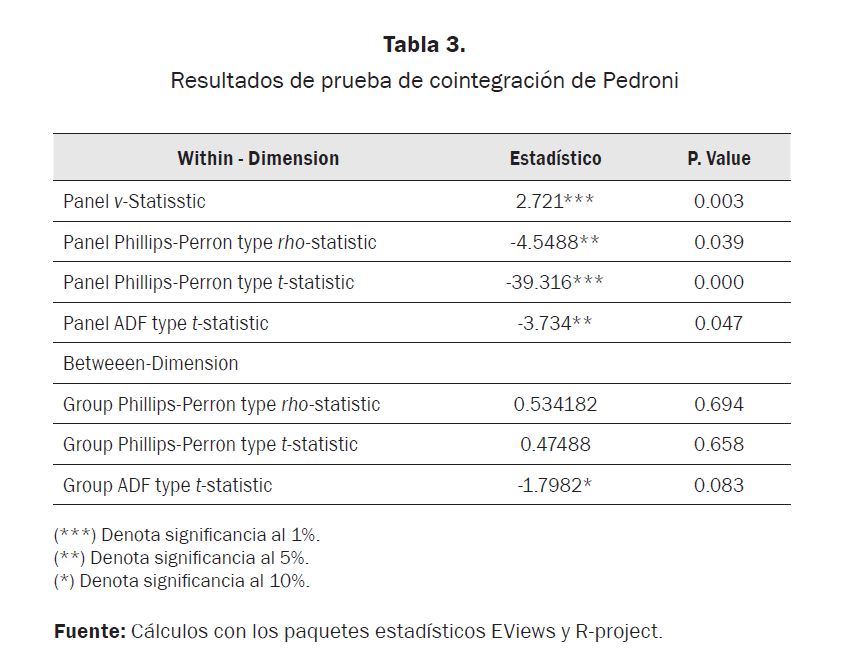

The main objetive of this research is to evaluate the long term relationship between energy consumption and GDP for some Latin American countries in the period 1980-2009. The estimation has been done through the non-stationary panel approach, using the production function in order to control other sources of GDP variation, such as capital and labor. In addition to this, a panel unit root tests are used in order to identify the non-stationarity of these variables, followed by the application of panel cointegration test proposed by Pedroni (2004) to avoid a spurious regression (Entorf, 1997; Kao, 1999).

Downloads

References

BANERJEE, A. (1999). Panel Data Unit Roots and Cointegration: An Overview. Oxford Bulletin of Economics and Statistics, S1(61), 607-629.

CAMPO, J. & SARMIENTO, V. (2011). Relación consumo de energía y PIB: Evidencia desde un panel cointegrado de 10 países de América Latina entre 1971-2007. MPRA Paper 31772.

DICHEY, D. & FULLER, W. (1979). Distribution of the Estimators for Autoregressive Time Series with a Unit Root. Journal of the American Statistical Association, 74, 427-431.

DICKEY, D. A. & FULLER, W. (1981) Likelihood Ratio Statistics for Autoregressive Time Series With a Unit Root. Econometrica, 49, 1057-1072.

ENTORF, H. (1997). Random walks with drifts: Nonsense regression and spurious fixed-effect estimation. Journal of Econometrics, 80, 287-296.

ENGLE, R. F. & GRANGER, C. (1987). Co-integration and Error-Correction: Representation, Estimation and testing. Econometrica, 55(2), 251-276.

GRANGER, C. & NEWBOLD, P. (1974). Spurious Regressions in Econometrics. Journal of Econometrics, 2, 111-120.

HADRI, K. (2000). Testing for Stationarity in Heterogeneous Panel Data. Econometric Journal, 3, 148-161.

IM, K., PESARAN, M. & SHIN, Y. (2003). Testing for Unit Roots in Heterogeneous Panels. Journal of Econometrics, 115, 53-74.

KRAFT, J. & KRAFT, A. (1978). On the Relationship Between Energy and GNP”. Journal of Energy and Development, 3, 401-403.

KAO, C. (1999). Spurious Regression and Residual-Based Test for Cointegration in Panel Data. Journal of Econometrics, 90, 1-44.

KWIATKOWSKI, D., PHILLIPS, P., SCHMIDT, P. & SHIN, Y. (1992). Testing the Null Hypothesis of Stationarity Against the Alternative of Unit Root. Journal of Econometrics, 54(1-3), 159-178.

LEVIN, A., LIN, C. & CHU, C. (2002). Unit Root Test in Panel Data: Asymptotic and Finite-sample Properties. Journal of Econometrics, 108, 1-24.

MADDALA, G. Y WU, S. (1999). A comparative study of unit root test with panel data y a new simple test. Oxford Bulletin of Economics y Statistics, 61, 631-652.

OZTURK, I. (2010). A Literature Survey on Energy – Growth Nexus. Energy Policy, 38, 340-349.

PAYNE, J. (2010). A Survey of the Electricity Consumption-Growth Literature. Applied Energy, 87, 723-731.

PEDRONI, P. (1999). Critical Values for Cointegration Test in Heterogeneous Panels with Multiple Regressors. Oxford Bulletin of Economics y Statistics, 0305, 9049.

PEDRONI, P. (2000). “Fully Modified OLS for Heterogeneous Cointegrated Panels. Advances in Econometrics, 15, 93-130.

PEDRONI, P. (2004). Panel Cointegration: Asymptotic and Finite Sample Properties of Pooled Time Series with an Application to the PPP Hypothesis: New Results. Econometric Theory, 20, 597-627.

PHILLIPS, P. & OULIARIS, S. (1990). Asymptotic Properties of Residual Based Tests for Cointegration. Econometrica, 58(1), 165-193.

SADORSKY, P. (2012). Energy Consumption, Output and Trade in South America. Energy Economics, 34, 476-488.

SOLOW, R. (1956): A Contribution to the Theory of Economic Growth. Quarterly Journal of Economics, 70(1), 65-94.

WESTERLUND, J. (2006). Testing for Panel Cointegration with Multiple Structural Breaks. Oxford Bulletin of Economics y Statistics, 68, 101-132.

Article Sidebar

Article Details

Authors who publish with this journal agree to the following terms:

- Authors retain copyright and grant the journal right of first publication with the work simultaneously licensed under a Creative Commons Attribution License that allows others to share the work with an acknowledgment of the work's authorship and initial publication in this journal.

- Authors are able to enter into separate, additional contractual arrangements for the non-exclusive distribution of the journal's published version of the work (e.g., post it to an institutional repository or publish it in a book), with an acknowledgment of its initial publication in this journal.

- Authors are permitted and encouraged to post their work online (e.g., in institutional repositories or on their website) prior to and during the submission process, as it can lead to productive exchanges, as well as earlier and greater citation of published work (See The Effect of Open Access).