Relación a largo plazo entre consumo de energía y PIB en América Latina: Una evaluación empírica con datos panel

Main Article Content

Keywords

Consumo de energía, crecimiento económico, función de producción, panel.

Resumen

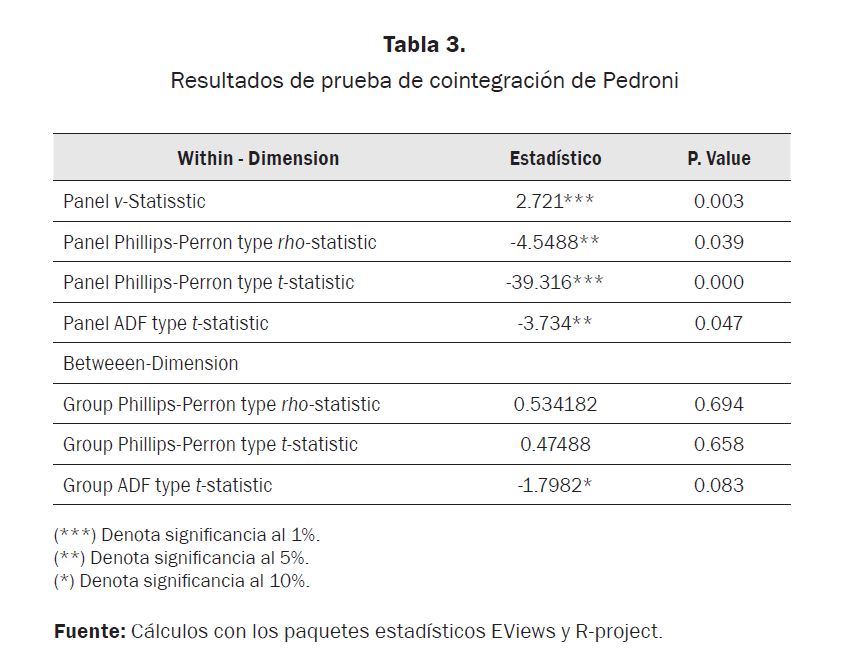

El objetivo principal de esta investigación es evaluar la relación a largo plazo entre el consumo de energía y el producto interno bruto (PIB) para algunos países de Latinoamérica en el periodo 1980-2009. La estimación se realiza con la metodología de datos panel no estacionarios, usando como forma de especificación una función de producción, con el objeto de controlar otras fuentes de variación del PIB como trabajo y capital. Con este propósito se utilizan test de raíz unitaria para identificar la no estacionariedad de las variables y el test de cointegración en panel de Pedroni (2004) con la finalidad de evitar una regresión espuria (Entorf, 1997; Kao, 1999).

Descargas

Referencias

BANERJEE, A. (1999). Panel Data Unit Roots and Cointegration: An Overview. Oxford Bulletin of Economics and Statistics, S1(61), 607-629.

CAMPO, J. & SARMIENTO, V. (2011). Relación consumo de energía y PIB: Evidencia desde un panel cointegrado de 10 países de América Latina entre 1971-2007. MPRA Paper 31772.

DICHEY, D. & FULLER, W. (1979). Distribution of the Estimators for Autoregressive Time Series with a Unit Root. Journal of the American Statistical Association, 74, 427-431.

DICKEY, D. A. & FULLER, W. (1981) Likelihood Ratio Statistics for Autoregressive Time Series With a Unit Root. Econometrica, 49, 1057-1072.

ENTORF, H. (1997). Random walks with drifts: Nonsense regression and spurious fixed-effect estimation. Journal of Econometrics, 80, 287-296.

ENGLE, R. F. & GRANGER, C. (1987). Co-integration and Error-Correction: Representation, Estimation and testing. Econometrica, 55(2), 251-276.

GRANGER, C. & NEWBOLD, P. (1974). Spurious Regressions in Econometrics. Journal of Econometrics, 2, 111-120.

HADRI, K. (2000). Testing for Stationarity in Heterogeneous Panel Data. Econometric Journal, 3, 148-161.

IM, K., PESARAN, M. & SHIN, Y. (2003). Testing for Unit Roots in Heterogeneous Panels. Journal of Econometrics, 115, 53-74.

KRAFT, J. & KRAFT, A. (1978). On the Relationship Between Energy and GNP”. Journal of Energy and Development, 3, 401-403.

KAO, C. (1999). Spurious Regression and Residual-Based Test for Cointegration in Panel Data. Journal of Econometrics, 90, 1-44.

KWIATKOWSKI, D., PHILLIPS, P., SCHMIDT, P. & SHIN, Y. (1992). Testing the Null Hypothesis of Stationarity Against the Alternative of Unit Root. Journal of Econometrics, 54(1-3), 159-178.

LEVIN, A., LIN, C. & CHU, C. (2002). Unit Root Test in Panel Data: Asymptotic and Finite-sample Properties. Journal of Econometrics, 108, 1-24.

MADDALA, G. Y WU, S. (1999). A comparative study of unit root test with panel data y a new simple test. Oxford Bulletin of Economics y Statistics, 61, 631-652.

OZTURK, I. (2010). A Literature Survey on Energy – Growth Nexus. Energy Policy, 38, 340-349.

PAYNE, J. (2010). A Survey of the Electricity Consumption-Growth Literature. Applied Energy, 87, 723-731.

PEDRONI, P. (1999). Critical Values for Cointegration Test in Heterogeneous Panels with Multiple Regressors. Oxford Bulletin of Economics y Statistics, 0305, 9049.

PEDRONI, P. (2000). “Fully Modified OLS for Heterogeneous Cointegrated Panels. Advances in Econometrics, 15, 93-130.

PEDRONI, P. (2004). Panel Cointegration: Asymptotic and Finite Sample Properties of Pooled Time Series with an Application to the PPP Hypothesis: New Results. Econometric Theory, 20, 597-627.

PHILLIPS, P. & OULIARIS, S. (1990). Asymptotic Properties of Residual Based Tests for Cointegration. Econometrica, 58(1), 165-193.

SADORSKY, P. (2012). Energy Consumption, Output and Trade in South America. Energy Economics, 34, 476-488.

SOLOW, R. (1956): A Contribution to the Theory of Economic Growth. Quarterly Journal of Economics, 70(1), 65-94.

WESTERLUND, J. (2006). Testing for Panel Cointegration with Multiple Structural Breaks. Oxford Bulletin of Economics y Statistics, 68, 101-132.

Article Sidebar

Article Details

Los autores que publican en esta revista están de acuerdo con los siguientes términos:

- Los autores conservan los derechos de autor y garantizan a la revista el derecho de ser la primera publicación del trabajo al igual que licenciado bajo una Creative Commons Attribution License que permite a otros compartir el trabajo con un reconocimiento de la autoría del trabajo y la publicación inicial en esta revista.

- Los autores pueden establecer por separado acuerdos adicionales para la distribución no exclusiva de la versión de la obra publicada en la revista (por ejemplo, situarlo en un repositorio institucional o publicarlo en un libro), con un reconocimiento de su publicación inicial en esta revista.

- Se permite y se anima a los autores a difundir sus trabajos electrónicamente (por ejemplo, en repositorios institucionales o en su propio sitio web) antes y durante el proceso de envío, ya que puede dar lugar a intercambios productivos, así como a una citación más temprana y mayor de los trabajos publicados (Véase The Effect of Open Access) (en inglés).